People learning economics are less likely to get into financial trouble

Kristoffer Balle Hvidberg

The financial crisis in 2008-10 showed that ill-informed financial decision-making among households have great consequences for the global financial markets. This has led to a growing interest in households’ financial behavior, in particular their debt behavior. Previous research shows that educational interventions can improve measures of financial literacy, but it has proven hard to show that this leads to changes in financial behavior, especially in the long term.

In a paper, which The Review of Financial Studies published recently, I investigate whether studying economics can reduce the risk of default and delinquency, and I find that admission to a Business & economics program reduces the risk of default 10 to 23 years after admission by one half (from around 10% to 5%). Is this just because a certain type of people choose to study economics, for instance, people who enjoy making budgets? If this is the case, it does not matter which study program they apply for because they have a low default risk no matter what.

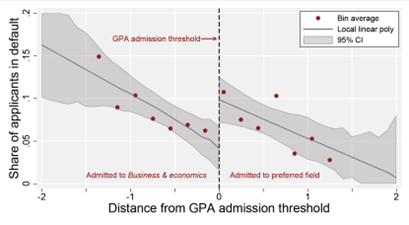

To rule this out, I exploit that the Danish system of admission to higher education generates unpredictable grade point average (GPA) admission thresholds. Imagine two very similar applicants. Both of them would prefer to study Political Science, but if they do not receive an offer to enroll in this program, they would like to study Economics instead. Due to a small difference in their GPAs from upper secondary school, only one of them receives an offer to enroll in Political Science while the other receives an offer to enroll in Economics. This means that one is just above the admission threshold for Political Science, and one is just below the threshold.

In other words, for the applicants I study, it is as good as random who studies Economics, and therefore the reduction of one-half of the default probability is the causal effect of admission to Business & economics programs.

But what about income? If economists have higher incomes, that could explain their lower probability of default. This is not the case, and at first, this may sound surprising. The explanation is that the applicants I study often would prefer to study Political Science or Law, and have Economics as their alternative. Since the income after graduation is high for all three of these programs, I find no effect of admission to Economics on total income, labor income, or rank in the income distribution.

Instead, I find that applicants admitted to Business & economics programs are less likely to owe money to their banks and are less likely to be liquidity constrained, which means they have higher deposits on their bank accounts, and therefore are more robust to economic shocks.

My findings show that economic education can reduce the risk of financial problems significantly and have long lasting effects on financial behavior. Thereby, my study serves as a “proof of concept” for smaller, scalable and more cost effective educational interventions aimed at improving households’ financial decision-making.

Figure 1: Admission to Business & economics programs and the probability of default

Notes: The figure shows how the probability of default and delinquency 10 to 23 years after admission falls from around 10% to 5% around the admission thresholds for applicants who have a Business & economics program as their alternative.

Hvidberg, K. B. (2023). “Field of Study and Financial Problems: How Economics Reduces the Risk of Default”. The Review of Financial Studies.